")

{kind=link}

milan2099/E+ via Getty Images

Investment thesis

My previous bearish call about Apple Inc. (NASDAQ:AAPL) kept up well until the company announced its record $100 billion-plus buyback plan. It was absorbed by the market with great optimism and the stock rallied by around 11% since then. However, to me, this buyback signals that the company likely cannot offer shareholders anything beyond it. Apple was well-known for its ability to create “Blue Oceans” during the Steve Jobs era, but it currently appears that the company struggles to differentiate and create brand new multi-billion industries. Products sales continue to decline across all offerings, as competition intensifies and the aggressively promoted Vision Pro did not fly, as I forecasted in my previous articles.

It also appears to me that the company is still not in an AI race. While other hyperscalers pour billions into AI data centers, Apple’s response has been to present a new iPad Pro for the market where competition is intensifying rapidly. Even the stock’s biggest fan, Warren Buffett, is aggressively trimming his stake in AAPL. I understand him, especially because my valuation analysis suggests that the stock is currently around 30% overvalued, which is a great selling opportunity. All in all, I downgrade AAPL to “Strong Sell.”

Recent developments

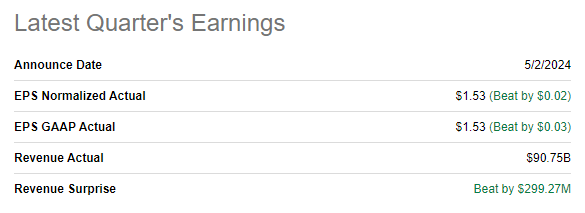

Apple released its latest quarterly earnings on May 2, when the company topped consensus estimates. Despite revenue declining YoY by 4.3%, the adjusted EPS expanded by one cent.

Seeking Alpha

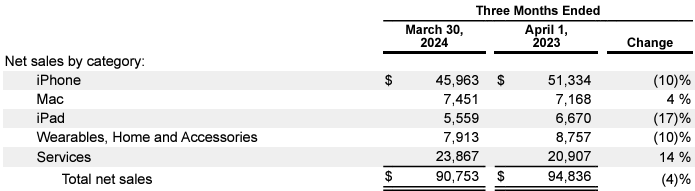

The market reacted to the earnings release with massive optimism because of the announcement of the record $100-billion plus stock buyback plan during the earnings call. Apart from this information, I think there were no more reasons for optimism. Fiscal Q2 showed double-digit YoY revenue decline in three out of five categories.

AAPL’s latest 10-Q report

In absolute terms, the Services segment once again was the only business line that delivered robust growth, almost $3 billion. Below $300 million YoY, revenue growth in Mac looks insignificant compared to the total quarterly revenue. The company continues exercising its pricing power in services thanks to its formidable brand name and customer loyalty. The latest increases in subscription fees were introduced in late October 2023, relatively recently. Despite Apple’s robust brand loyalty, I doubt that increasing subscription fees any time soon is possible without undermining customers’ sentiment. Therefore, momentum in Services revenue is likely to start cooling.

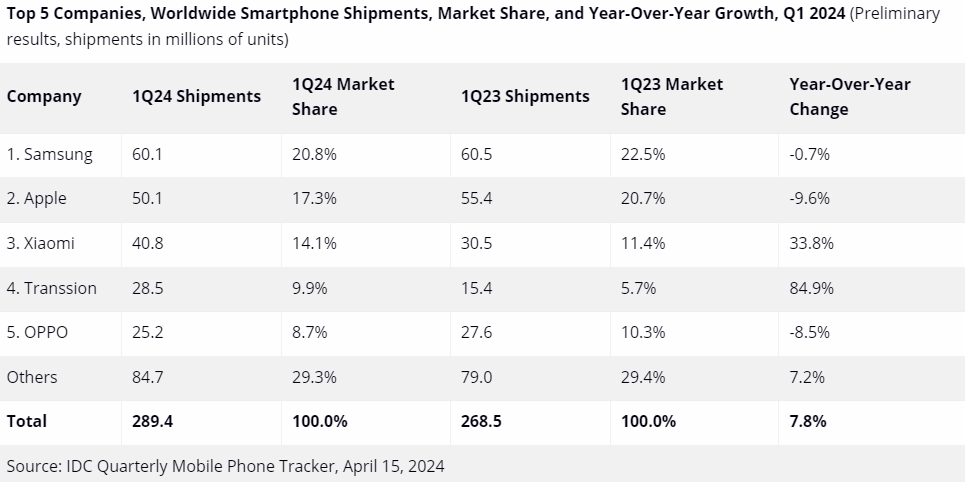

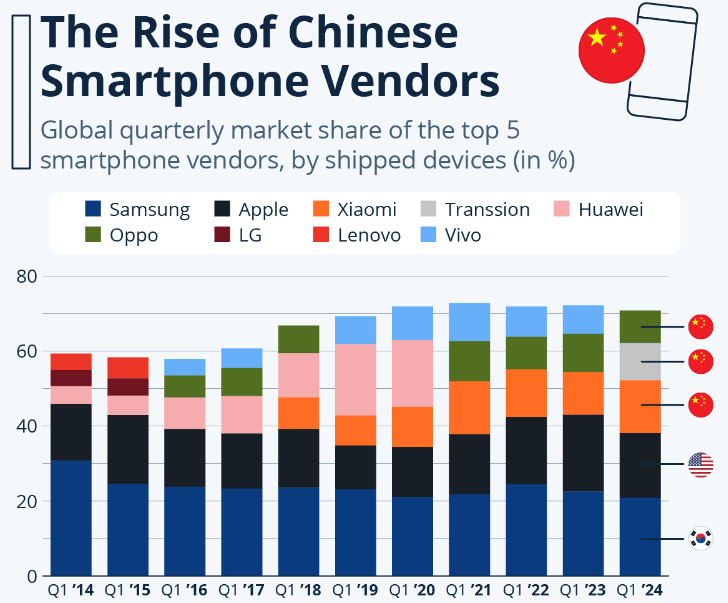

Apple generates more than half of its revenue from the iPhone. And this revenue stream has been struggling for several past quarters. According to IDC, Apple’s market share has shrunk significantly in calendar Q1 on a YoY basis. The market share dropped from 20.7% to 17.3% YoY, which is the worst performance among the top five vendors.

IDC

The global leader in smartphones, Samsung (OTCPK:SSNLF) also demonstrated a market share decline in Q1 as Chinese manufacturers are gaining momentum. The competition in smartphones intensifies rapidly and Apple even introduced 20% discounts for iPhones in China. Such a deep discount helped to show China iPhone sales rebounding. To me, this indicates that Apple fails to differentiate itself from competitors. This is a warning sign because Apple has traditionally been at the forefront of the smartphones’ premium segment, that is, the differentiation was its key to charging premium prices.

Statista

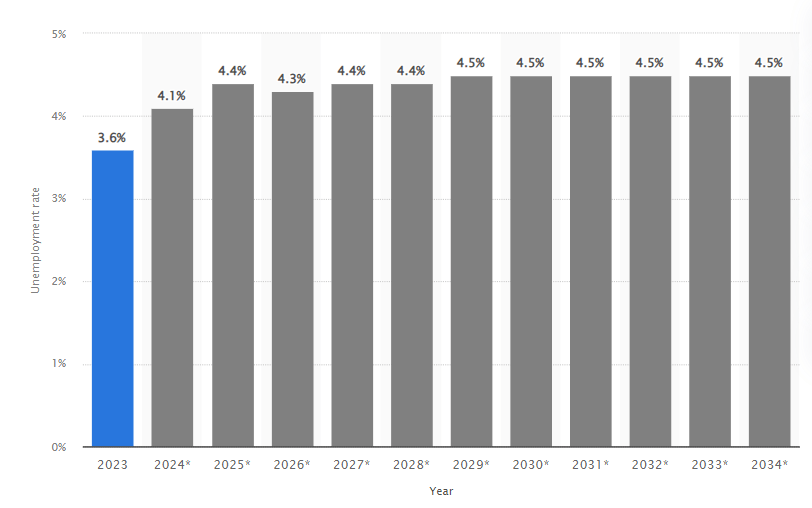

With interest rates likely to stay higher for longer, there is the risk that discretionary spending will be soft. Moreover, unemployment is projected to grow in the U.S. for two years in the row. This also does not add optimism for discretionary spending and will likely lengthen iPhone replacement cycles.

Statista

Smartphone industry is not the only where Apple suffers from rapidly intensifying competition from Chinese vendors. According to Statista, Apple’s market share in tablets deteriorated notably on a QoQ basis in Q1, from almost 41% to 32%. Meanwhile, Huawei’s market share in tablets expanded from 7.6% to 9.4%. Apple recently unveiled new iPad Pro with a powerful M4 chip suitable for sophisticated AI applications, which might help to differentiate and regain market share. However, intensifying competition in tablets is also a risk for Apple’s investors.

Apple’s Vision Pro did not become a banger, as I forecasted in one of my previous articles about the company. According to Ming-Chi Kuo from TF International Securities, Apple has reduced its yearly forecasts for the headset to between 400,000 and 450,000 units, down from original projections of up to 800,000. The product has been aggressively promoted, and such a downgrade in the forecast is a big disappointment.

Finally, it appears that all Apple’s secular challenges are apparent to one of the greatest investors in history, to Warren Buffett. Mr. Buffett has significantly trimmed Berkshire’s (BRK.B) stake in Apple in recent quarters, which is also a red flag for investors, in my opinion. Berkshire’s stake in Apple is still massive, but reducing its stake for two quarters in a row is quite a trend.

Valuation update

The stock lags the broader market, which is fair given all the fundamental challenges AAPL faces. The stock price rose by around 9% over the last 12 months, compared to a 26% rally in the S&P 500. On a YTD basis, Apple is approximately flat, while the broader market gained around 11%.

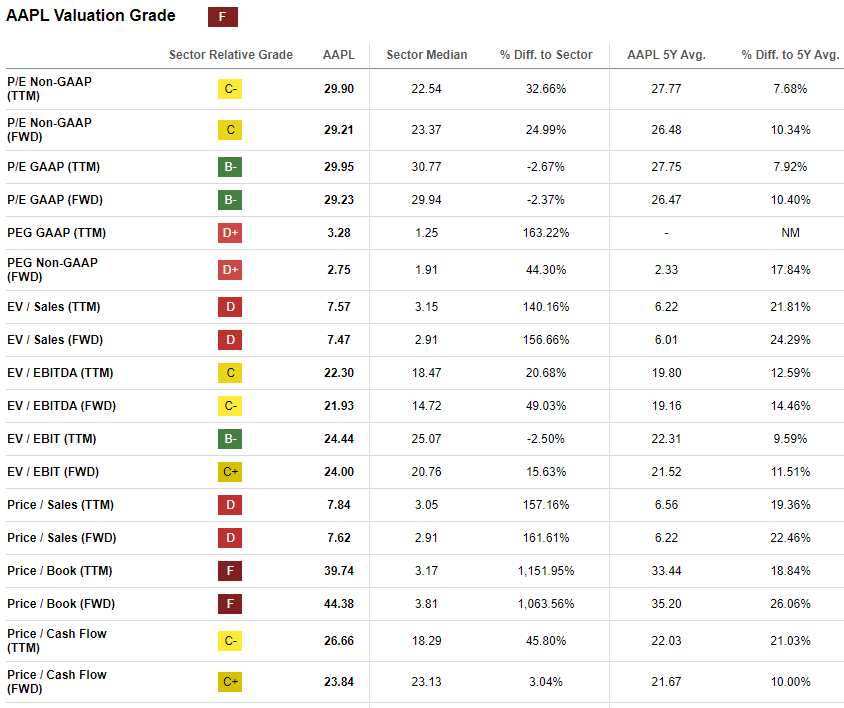

Apple’s valuation ratios are always much higher than the sector median, but it is fair given the company’s scale and profitability. Therefore, it is better to compare current multiples with historical averages. From this perspective, AAPL looks overvalued, as its current valuation ratios are higher than the last five years’ averages across the board.

Seeking Alpha

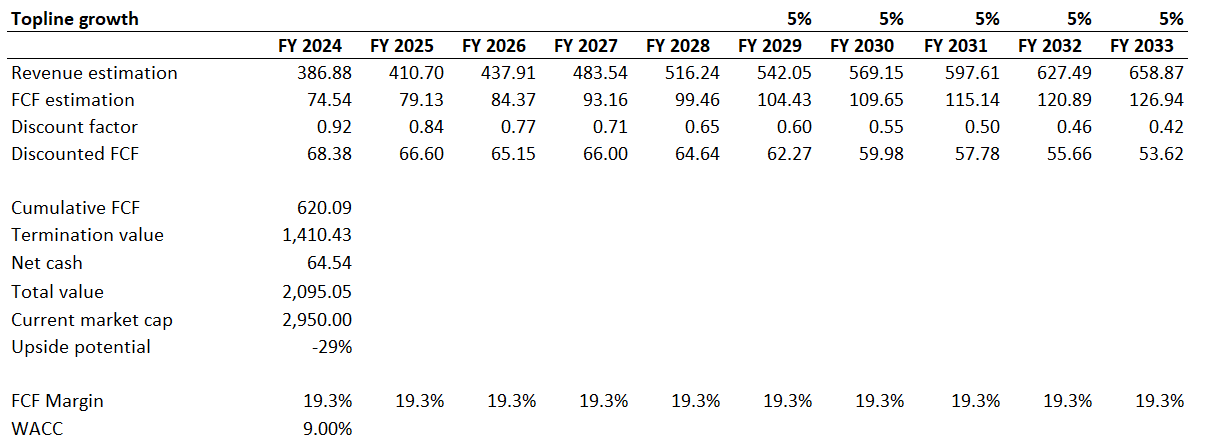

To determine the extent of overvaluation, I must simulate the discounted cash flow [DCF] model. A 9% WACC is close to the level I used previously, and it aligns with the range recommended by valueinvesting.io.

Revenue consensus estimates are available for the next five years. With around $400 billion annual revenue, the company faces a big “law of large numbers” problem. Therefore, I project a modest 5% revenue CAGR for the years beyond FY 2028. Due to all the secular challenges AAPL faces, I do not expect AAPL to expand its 19.3% TTM FCF ex-SBC margin.

Author’s calculations

According to my DCF simulation, the business’s fair value is around $2.1 trillion. This is almost 30% lower than the current slightly sub $3 trillion market cap. Therefore, AAPL is substantially overvalued, based on my assumptions.

Risks to my bearish thesis

Betting against one of the most successful companies of the 21st century is extremely risky. Apple has vast financial resources to hire the best people and brightest engineers which will be able to deliver a new jaw-dropping product. Vision Pro’s failure suggests that there is a creativity crisis in Apple, but for one of the largest companies in the world, there is always a probability to make a stellar comeback.

As Warren Buffett once said, the stock market is a voting machine in the short run. This means that the share price significantly depends on noisy headlines and sentiment. The recent rally after announcing a record buyback package proves this theory because earnings analysis suggests that there are no reasons to be bullish. That said, this buyback-driven rally can last for a while.

The upcoming important event from Apple called WWDC 2024 might be another positive short-term catalyst for the stock price. During the event which will be held next week, the company is expected to unveil the new iOS 18 and experts expect that the company will incorporate generative AI features into it.

Bottom line

To conclude, Apple’s stock is still a “Strong Sell” to me, especially after the recent rally. There were no positive developments apart from the record buyback plan and releasing the new iPad for the market, where competition intensifies rapidly. Apple’s secular challenges are apparent to me, and it appears that even the stock’s biggest fan, the great Warren Buffett, recognizes these threats. The stock is significantly overvalued, in addition.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.